Those poor millionaires, being asked to contribute to society. How could you?!

Hey. These hard working millionaires are tricking this money down by buying stocks and investing in real estate and then upping the price of rent to continue to increase their wealth so they can push to the next tier of millionaire".

Which they’ve hired accountants to do for them. But I assure you, their work lunches are exhausting

Reposting from another thread:

Social security has been 10-15 years away from being insolvent for 80 years. It will always be 10-15 years away from being insolvent because of the way it’s calculated.

When the CBO or whoever scores it they can predict certain things like the number of recipients, the size of their payments, and inflation. They aren’t allowed to take into account things that Congress may (but definitely will) do in the future, like raising the cap on social security taxes roughly with inflation. It went up from $160200 in 2023 to $168600 in 2024. This is a rare bipartisan, uncontroversial thing. Congress almost always follows the SSA recommendation exactly.

It would be more accurate to say “if the social security cap stays at $168600 for 10 years, social security will be insolvent.”

The people pushing this bullshit know it’s bullshit. They do it to make people think they’ll never get social security so they can get enough voters on board with killing it, like they’ve been trying to do for 88 years.

Don’t fall for it.

Apologies, but your specific example is incorrect. The cap on social security taxes is adjusted every year not by act of congress, but by existing law that indexes the cap to inflation. Therefore, it is already baked into the way it is scored and is not ignored.

You are correct that scoring cannot take into account any actions congress may take.

This time is a little different though than history. From 1984-2020, Social Security took in more in revenue than it paid out on benefits. It is now running at a deficit. Since being formed, it has run at a deficit less than 15 total years, and most of them earlier on. The social security trust fund has never been depleted during that time either. Without any changes to law, it will continue to run at a deficit until the late 2030s when the trust fund would be depleted and taxes alone would cover a projected 80% of benefits.

That 80% is why it’s bullshit to your point. There are so many simple, easy ways to solve this and if they do nothing, we could continue to pay out 80% of benefits with no other changes but that’ll never happen. It would be political suicide to literally starve our retired population. My favorite way to address it is removing the cap, but there’s other small adjustments that make a huge difference. Things like changing the inflation adjustment to a similar but lower index, raising the retirement age, raising the tax by less than a percent, means testing, etc … and the thing that pisses me off is the sooner we take one of these actions, the more of the trust fund is preserved, and the impact is so much greater. I don’t like the other solutions and would strongly prefer raising the cap, but I’d take most of them over inaction, depleting the trust fund, and reducing benefits.

I was trying to keep it short and simple by skipping a step but yes, the SSA follows a formula to raise the cap. But anything the executive does must be authorized by Congress, including the current formula which was set in a reauthorization bill back in the 80s (I think, maybe the 70s, apologies, but I’m not able to look it up right now). So far, every time a budget is passed and every few years when the SSA needs to be reauthorized, they’ve left them alone. Despite the occasional bill messing with the SSA getting introduced, they never get out of committee.

As far as the CBO goes I don’t recall ever reading about cap increases in their report summaries on the trust fund. Although I have read their reports on the effect of various proposed changes to the way the cap is calculated. I’ll have to do some more looking when I have the time, but I was definitely under the impression cap increases were in a category the CBO didn’t anticipate future changes to when evaluating the health of the trust fund. I thought normally the COLAs would also fall into this category but that is overridden by them being mandatory spending, as opposed to discretionary, so they have to be taken into account. I’m certainly no expert and wouldn’t be surprised to find out I missed something.

It’s still time to scrap the cap of $168,600 income that has to pay in. Pay the full amount on all our income, or GTFO of the US.

Says the kender? An entire RPG culture based on “innocent” theft and misappropriation? Hunh.

edit: Ah tes, the downvoters are, yet again, too young to know better. When will Reddit stop leaking? 🤦🏼♂️

Ok, I will engage as a Kender.

First of all, me calling myself a Commie is actually superfluous here as evidenced by the Siberian natives that were so damn communist that the USSR couldn’t deal with them.

Secondly, the fact that you use the artificial concept of ownership to describe Kender society, shows that you know nothing of Kender. We own nothing, we don’t understand ownership at all, unless you big folk explain what you mean.

The biggest crime one can commit as a Kender is not having children. That comes because we are afflicted with wanderlust. I’m a perfect example of this having lived in 49/50 states in the US, and planning to “‘retire’” on a ship that I own, but pay for with charter cruises to everywhere else I can get to. I digress.

If you don’t return to Kenderhome by your 60th birthday and have at least two children with your council chosen betrothed, or a romantic partner, then we will dispatch bounty hunters to bring you back, alive, and deposit you in the “palace” of Kenderhome. You are then on house arrest, and not able to leave the grounds. This is possibly the worst possible punishment one could give a Kender, other than solitary confinement, thankfully all your locks are trivial for us to pass through, so no one has ever held a Kender in solitary confinement.

The Kender on the whole are an annoyance to those of you primitive races that understand the concept of ownership, but that’s not our fault. You should learn the concept of belonging.

Edit, I didn’t downvote you.

Edit 2: I’m less than 20 years from having to have podlings, if Krynn has a direct connection to us.

Edit 3: while I have created a Hoopak and a Chappak, IRL, I don’t own them. If you need to borrow the Hoopak, or the Chappak,.or pretty much anything else in my possession, I will happily lend it to you, knowing you’ll give it back to the community as good, or better, than you got it. It’s a real shame I can’t rely on normal humans to do the same.

Edit 4: All Weapons should also be tools and musical instruments.

Edit 5: Yes I’m an angry Kender. We only use money because you force us to. We have/had a society that works so damn well the biggest issue we have is forgetting to have kids. I’m extremely disappointed in the lack of progress, despite the insane amount of wealth that human society has produced.

Ah, the inherent sovereign citizen BS in kender “culture”. Color me surprised.

Hardly. You’re too big to understand us little folk.

That’s populism, and left populism is pretty strong here.

Your logical fallacy is showing, and your comment is wholly bullshit. Bye, Felicia.

True men of culture watched the credits and know it’s spelled Felisha.

They spend more as they get in, it will run out. No amount of tomfoolery will change that.

They’ve been saying that my entire life, my dad’s entire life, and when my dad was my age, my grandfather would tell him he’s heard the same things his entire life going back to the 40s.

For a couple decades the disingenuous doom -and-gloomers told us no way could social security ever deal with the baby boomers. All through the 80s and 90s they told us we might as well privatize it or kill it all together. The only time wall street shut up about it was when they were too busy jerking off to the thought of getting their hands on that money. Well, the youngest of the boomers turn 60 in '24, they’re almost all in and the end times keep getting pushed back, from the 80s to the 90s to the 00s to the 10s to the 20s and now 2035. It’s like a doomsday cult that keeps pushing the date when the apocalypse doesn’t arrive at the appointed time.

You’ll have to excuse me for not getting worked up over the 40th new year I’ve heard for the sky falling.

And for what it’s worth, managing the COLAs, the cap, the percentages, and anything else the SSA has done throughout it’s existence isn’t “tomfoolery,” it’s accounting. And damn good accounting so far. The SSA being such a well run government institution probably makes republicans hate them almost as much as the tax itself.

LOL, just posted the same, but not nearly so learned or eloquent.

KIDS: You’re getting your Social Security. And remember, us old folks are not going to go senile and vote against it!

It’s called the “third rail” of American politics for a reason. Touch it, you die.

Sure upto now it’s been fine…

But a WHOLE LOT of new people will be getting check soon…

And military and debt spending are through the roof And the normal people are paying groceries and rent with their credit card…

I’m. Sure they’ll solve it tho, last minute.

That exact comment would be at home in a letter to the editor in response to an article in any newspaper, in any year, for the past 80 years. And on any discussion board from the earliest days of the internet until now.

I’m not going to make any assumptions about your age or the length of time you’ve paid attention to these issues, but if it’s only been a decade or so, you should start seeing the pattern soon. It won’t even be at the last minute, it’ll just keep slowly moving out so it’s always 10-15 years away. Don’t let them scare you into helping them do what they’ve been trying for 88 years.

This program has kept a lot of elderly and disabled people out of poverty. Don’t let them take it.

deleted by creator

-

No.

-

“Tomfoolery”? Step away from the idiot box, gramps.

Sure granny, go believe them,I’m sure those 2 trillion arnt in some loss leading 1% government bonds

Have you not been paying attention to what the Fed has been doing? Pardon my language but shoving cash up my asshole earns more than 1% these days.

In 2022, before most of the rate hikes, the trust fund earned $66.4 billion. This year’s high, and hopefully very temporary, interest rates aside, it’ll usually be around 2.5-3%.

I’m not sure what you think loss leading means or why you’re using it here, but governments storing reserve money earmarked for a specific purpose in their own bonds isn’t unusual or a bad thing. Should they stuff it under a mattress earning 0%? Should they risk it in the markets? Unsecured domestic bonds? Foreign bonds?

Sorry, I must admit I’m not from the us and I may have been more talking/afraid for my local governments funds… Thanks for the great explanation tho!

So pissy you can’t even type straight? Breathe, tiger. Go touch grass.

Now you’re cheating, cause that would be good advise always.

-

The current trust fund is > $2T.

It is not going to “run out”. That is republican talking point and propaganda. God damn that myth is believed by everyone.

The concepts of solvency, sustainability, and budget impact are common in discussions of Social Security, but are not well understood. Currently, the Social Security Board of Trustees projects program cost to rise by 2035 so that taxes will be enough to pay for only 75 percent of scheduled benefits. ^1

75% of benefits will still be paid in even the worse case scenario. The fear mongering is not necessary.

GenX here. Got some free financial advice in 1993 or so. Asked about Social Security being cancelled because my entire class ('89) said we didn’t expect to receive it.

She looked me straight in the eye and said, “No. There will be riots in the streets before Social Security is cancelled. This is a non-issue, you’re getting it. Any other concerns?”

GenZ, 30-years later, “We’re gonna get cancelled!”

No fuck you won’t. Old people vote. Isn’t that what they’re always bitching about? Think we’ll shoot our retirement straight in the skull?!

Also Gen X, graduated in '96, and was warned by my econ/government teacher that we need to have well funded IRAs, because we won’t be getting enough social security benefits to even pay for food, much less rent, medicine, or healthcare.

This is what they mean when they say Social Security is basically bankrupt. It won’t pay for shit, and I live with people who currently draw on SS. It already doesn’t even pay the 1/3 of their retirement it was supposed to. We don’t get the retirement plans (pensions) from the companies we work for that was supposed to cover that last 1/3 of our retirements.

It was supposed to be a three-pronged plan: Social Security, 401k, and corporate pension. Each of these has problems on their own, but a hybrid solution could cover for each other’s issues.

Now, corporate pensions are rare, 401k’s are highly vulnerable to stock market crashes, and Social Security is being slowly strangled.

401k’s are highly vulnerable to stock market crashes

not really. short term investments and speculation are vulnerable to short term market forces, but a 401k that sits for 30 years with regular contributions and profits reinvested is all but guaranteed to make money. Long term investments like that are extremely stable, just put the money in your 401k and don’t look at returns until you’re actually considering retirement.

What’s critical is where the stock market is at when you retire. Stock market crashes coming with general economic problems mean older people lose their jobs, can’t find another one, and are forced to retire with 40% of their 401k value knocked out. This is exactly what happened to people in 2008 and '09.

Conversely, the stock market did really well in the years after that. The people who were able to hold out past 2012 were able to get a nice nest egg saved up.

It’s a dice roll. It can work as one part of a larger system, but not on its own.

40% of their 401k value knocked out

40% of the value before the crash, I assume? In that case, what’s the difference between their contributions and the total value even with that 40% gone? Remember that the real value of an investment is how much money is there now vs how much you put in, not how much money is there at peak value vs how much money is there now.

Most corporate pension for workers are a joke. All the money goes to the top few.

401k’s are highly vulnerable to stock market crashes

No problem, just make a self-directed IRA that buys bitcoin. Immune to stock market crashes!

Social Security is being slowly strangled.

The demographics are probably a bigger part of it. The ratio of people collecting to people paying in is much larger now and the length of time people collect on it is longer since people live longer now.

!remindme 20 years

Now, that’s optimistic. 🤣🤌🏼

However we do have the worst case scenario of 75% of planned hanging over our heads. In the next ten years or so, either we’ll take a big hit on income or there will be painful changes to prevent it. I don’t like either of those. Like everything else we can’t seem to do, the best fix is to do it ahead of time to greatly reduce the impact. It is important that Congress get off their asses and address it now so whatever adjustment will hurt less.

Previous adjustments have included raising the cap, taxing more benefits, raising the retirement age, and changes to the formula for cost of living adjustments. We really ought to consider a balance of all those and more so we spread the pain

They will make laws to change it but grandfather in people born before a certain age

I know this is false because I’ve looked into how it works, and it still makes me feel sick to hear every time. Of course, the truth is bad enough, we don’t need to lie.

“I only robbed you of 25% of your income, what are you complaining about?”

What people mean when they say “run out” is that it won’t be able to keep up with its obligations. That is objectively bad. People will get reduced payments. There will be pain.

You are just changing the definition of words so that your new meaning lines up. Which I guess is one way to approach the argument. But not necessarily a helpful one.

Please see my comment here.

No, it isn’t. That’s bullshit, a talking point designed to get you to give up on supporting it politically.

But do you know what would help it in actuarial terms? 2 things:

-

raise the federal minimum wage

-

remove the cap on income subject to the social security tax

When suppressing wages became a bipartisan affair, it hurt Social Security just as much as it did workers on the low end of the wage scale.

Also make the SS fund separate from the general fund and make the general fund (aka the military) pay back what they took from SS originally.

-

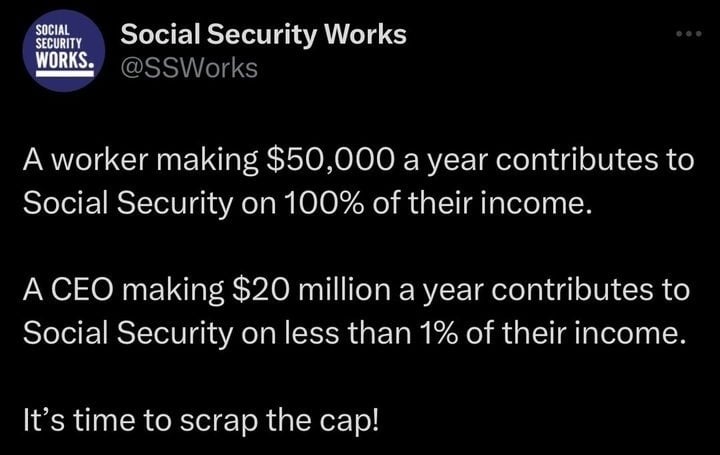

$168,600

That’s the cap. It is clearly and obviously only benefiting the rich. Absolutely insane.

It also benefits the upper middle class. And middle class in HCOL areas.

It should be adjusted based on cost of living.

Making $150k in NYC is like making $50k in middle america.

Is this accurate?

deleted by creator

I think you’re missing the point. He wasn’t saying that $50k is a lot in middle America. The point was that $150k in New York is also not much money.

I literally do not care about the upper middle class.

👍

Removed by mod

Lazy-ass boomers that paid into SS their entire lives? Those lazy-ass boomers?

Yup, the same ones that actively were able to benefit from the cap of ss contributions due to their secure jobs paying out more than any of us are proportionally making now. Those same secure jobs they only received because the U.S. got to establish itself as a global hegemony due to being largely unharmed by WW2.

Boomers got to live the good life at the expense of our future, and they didn’t do a goddamn thing to deserve it.

In my market, the median cost of housing has risen over 600% relative to median income since '74 - they’ve ridden that wave at the expense of future generations after breaking the guardrails off the economy. They haven’t paid their fair share into SS, and now they’re demanding more.

I thought millennials were supposed to be selfish and lazy.

Like millennials, right?

What happens when social security does run out and the millennials and gen z who have paid into it for years get 0 benefit? Ok, we’ve helped the boomers retire. But then when we need it it’s not going to be there.

Only if we let the GOP and MAGAts control the narrative and make people not understand that minor reforms can make it feasible for DECADES longer than the projected 2035 at current funding rates. But people are stupid and greedy, which is (one reason) why the GOP still has as much power as they do.

The cliff has been looming for decades, and neither party has done a damn thing about it. It’s fine if you want to blame the MAGA circus, but the truth is that no politician is going to do a damn thing until we hit a point of no return. The solutions are incredibly simple, but they all start with raising taxes, so no party is even going to bother.

These dumbasses call me a boomer. My parents were boomers.

All you gotta do to score some upvote dopamine is throw that word out there. Score!

And yes, Boomers, GenX, Millennials and GenZ, all of us deserve what we were promised. And we will get it. Won’t be enough without some work and planning during one’s working years, and won’t be as fair a deal as the older folks got, but Social Security is going no where.

Removed by mod

Our (I’m from UK) governments are so fucked up every decision is to make the rich richer. At this point I have no idea how the western world can break out of this corruption

Everybody unionize?

I work for a private wealthy company and have no issues personally with money. Is it my responsibility to quit this job and get a lower pay one to unionize?

Honestly I’m genuinely lost on how to help everyone else. I guess the issue is I’m not selfless enough to give up my lifestyle or money to help.

I have voted for labour (or any other party besides the Tories) every single local and general election. That’s pretty much all I can do

Without knowing the specifics of your situation, I’d suggest maybe keeping your existing job, but talk to your coworkers. Start by discussing salary, and then work your way up to possible unionization. You shouldn’t have to be selfless; that won’t scale.

I can somewhat relate - I’m an engineer and only a handful of us at my company seem interested in unionizing.

That’s exactly right. They did that because they don’t need it and don’t want to pay into it. Our education system is horrible, imagine if people without kids in school were able to just not pay into the education system? This is the same as that.

Everything else aside, social security is not going to run out in 10 years, all the doomsday is if we do NOTHING, but we never do nothing on social security. It’s not going to end or “go bankrupt”, this is all fear mongering BS that doesn’t stand up to the smallest dose of objective reality.

To make SS solvent all they need to do is make higher income earners contribute on the same scale they make lower income earners pay already.

If people making above 140,000ish had to keep contributing at the same rate as everyone UNDER that number does, there would be no issue at all. But a billionaire pays as much into SS as someone making 140k a year, probably LESS because of the Social Security payroll tax income limit.

Tax the rich already!

Eat them, but ok.

I’m good with either.

Libs going to lib

This never made sense to me. You get out of Social Security more or less what you put into it (with lower income earners actually getting a bit more, proportionately speaking). If you remove the cap, people will be paying more into it now and pumping the fund up. Eventually, we just hit the same problems when those high income earners eventually withdraw, since they’ll be pulling that much more, as well.

I get the “tax the rich” idea, but Social Security isn’t a tax, at least not in the same way as everything else. It’s a retirement fund with mandatory contributions.

If you look into bend points, you will see that the first amount you contribute gets you a significant return later for your SS check, but as you contribute more, the slope of the size of the SS check flattens. After the second bend point, adding more into SS doesn’t get you a much larger check.

The reason the rich wouldn’t want to further contribute then, is because at that point, their contributions are getting a very poor return, and they would feel they could do better on their own. Since it isn’t a tax, they would argue (correctly) that it is a waste of their money compared to investing themselves.

it’s not gonna run out.

it will be far worse, we’ll all pay into social security and when we get it back it won’t cover the cost of your monthly bread ration.

Stop spreading this BS. SS going bankrupt is misinformation.

I want to believe. Can you provide sources for that claim?

How about OP provides sources to their claim first.

On one hand: fair. If you’re not versed in elements of tax law this bit of data can seem arcane.

On the other: this is a matter of policy - not one of research. The definitive answer can be found with relative ease via a Google search. Here’s a link to a Social Security Administration page on the topic: https://www.ssa.gov/OACT/COLA/cbb.html

By the math set out at the above link, one can calculate that, at a maximum income of $168,600 and a SS Contribution rate of 6.2%, the most any individual would contribute to social security in a year would be $10,453.20.

$10,453.20 would represent 0.052266% of the income of someone making $20 millions per year. Even doubling that amount (as some conservatives do) to count the employer’s contributions to Social Security would leave you with just over 0.1% of net income.

So yeah, even if Social Security isn’t going bankrupt, it’s an anemic system that barely provides livable circumstances for those who depend on it. Raising or removing that “max income for contributions” limit would go a long way to seeing the system be able to actually support people who need it while only burdening those most able to bear the burden.

Ninjaedit: grammar

Is it though?

(From Bard) “The Social Security trust funds are projected to run out of money by 2034. This means that the Social Security administration will only be able to pay out 77% of a retiree’s full benefits.”

Which I get isn’t exactly the same as what OP is claiming, but it is still pretty concerning for those of us not close to retirement age

Read any SS Trustees report. It doesn’t have “money”, it has debt instruments (bonds), which are essentially a document saying “we the government owe ourselves a thousand dollars”. You can print those all day, it’s only sourcing that money that has any kind of direct consequence (taxation, inflation, etc.).

And yes, that does raise an interesting question of, what did they do with the actual money we paid into the programs, if the only thing in the trust fund is bonds.

Don’t they pull from SS funds to pay for other things but then “give it back” at some point? I feel like I read something about that, maybe what’s being paid back isn’t “cash” but bonds?

In effect, the bonds I mentioned are just inverted loans. The Treasury takes in $1k from payroll taxes for these programs, issues a bond to the trust fund saying “I owe you $1k plus interest”, spends the $1k on whatever (I guess primarily the discretionary budget) and eventually has to somehow generate money to pay it back with interest.

In terms of whether or not bonds were “borrowed” - this wouldn’t exactly matter in a meaningful sense, but I’m not clear this ever actually happened in the first place. There was some claim about, when the trust fund was mixed with the general fund 1968-1990, maybe the government took bonds out of the program, but you have to remember that inside the government, that’s not something of value, that’s just an obligation the government has to pay to itself, it’s a big nothing burger. The outstanding liabilities from Social Security to the actual beneficiaries (elderly people) exist regardless of how the government is doing their accounting internally.

is still pretty concerning for those of us not close to retirement age

It’s even more concerning for those of us who are close. Even most of us with savings are pretty reliant on that for retirement

Isn’t “exactly” still means the statement “bankrupt” is false. Don’t move goalposts in the claims. That’s disingenuous and only adds to the misinformation.

not just social security. top income tax bracket is at the begining of 6 figures and of course there is a discount to corporate tax rates and if you don’t make your money through labor.

Yeah why is there a benefit for people who don’t make their money from labor? They need to be rewarded for already making more by doing nothing? Nonsense

Are you legitimately asking?

Because they pay politicians to make it so.

What is the difference between a CEO and Santa Clause?

spoiler

Both of them judge you all year round, but one of them performs at least one day of work.

SS Works is

A poorly thought out tag

Could someone explain how it could run out if there are still workers contributing to it every year?

deleted by creator

Ah thanks! This explained everything.

Because it’s paying out/getting raided faster than people are contributing to it

Population contraction and major shifts in wages compared to cost of living.

deleted by creator

Who would opt out of SS the most? People living paycheck to paycheck. Who can’t save for retirement at all? Those same people.

Allowing an opt out would mean homeless and suffering old people wandering and dying in the streets. Which is why SS was created in the first place.

deleted by creator

Absolutely 1000% no.

Social security is guaranteed by the federal government. Making social security into 401k only benefits corporations by giving them a guaranteed funding source.

Hell, I hate the fact that companies moved from a pension system to 401k. Social Security is one of the last places where we have guaranteed income.

Social Security is adjusted for inflation and provides a predictable income stream you can plan for. Having it tied to the stock or bond market would result in big swings and also potential loss. Social Security isn’t maximized for profit, it’s maximized for predictability.

No.

I don’t think they were confused by your point, as the idea is bad on its face for the very reasons they noted.

Plus you could leave it to your heirs if you don’t spend it all, whereas your heirs over age 18 get nothing from SS after you die except a laughable few hundred for funeral expenses.

deleted by creator

Paul Krugman has an excellent book that spends the first few chapters discussing social security and the GOP’s dream of privatizing it called, Arguing With Zombies. I recommend checking it out, it covers a lot of US economic topics and dispels many myths.

But really, much of the drama around SS is very overblown. A small reform of increasing SS tax from 12.4% to 14.4% will fund the program for the next 75 years. Source: https://www.ssa.gov/policy/docs/ssb/v70n3/v70n3p111.html

The reason it’s even having a funding issue in 12 years is due to Congress (primarily the GOP) refusing to make the necessary reforms. They want it to fail because they want to privatize it, which Paul Krugman’s book goes into great detail about. Additionally, the average birthrate in the US went from 3 children per woman to 2 children, meaning there are less people paying in than before. And again, this is easily fixed by simply raising the tax by 2% (or lowering benefits by 13%), which the link I provided earlier discusses.

Getting rid/allowing people to opt out of SS is a terrible idea. Yes, many folks could take that money and have a better return. However, the majority of people would not. And what would happen when they’re disabled or retirement age? They’d be fucking broke and have zero savings. Guess what happens then? Mass crime. Crime like you’ve never before seen in the US. Social programs have proven time after time to be more effective at preventing homelessness and crime than any other government policy. Getting rid of it or even allowing people to opt out would 100% backfire on society at large.

As someone who hits the cap and lives in a place where even monthly premium payments for our healthcare have been scrapped, I am really sure it’s time to open up BOTH of them again.

Sure, it’s a cost. Sure, it’s less cash in my pocket. But holy hell, we need to keep the cash going into the system so the next right-wing nutters can’t gut the services via some “fiscal responsibility” bullshit.

{kind=link}